What are some of the things you should look for when selecting the right bank fees

I’ll be honest: bank fees are one of those topics that sound boring right up until you pay one. Then suddenly you’re very awake, doing mental math, asking yourself why a tiny mistake turned into a $30 problem.

This cluster article is meant to make that less likely. If your goal is to choose a bank you won’t regret, the fee structure matters as much as the interest rate, the app, or the number of ATMs on the corner. Maybe more.

And if you want the big-picture context first, it pairs with the guide here: what are some of the things you should look for when selecting the right bank?

Why bank fees feel “random” (and why they aren’t)

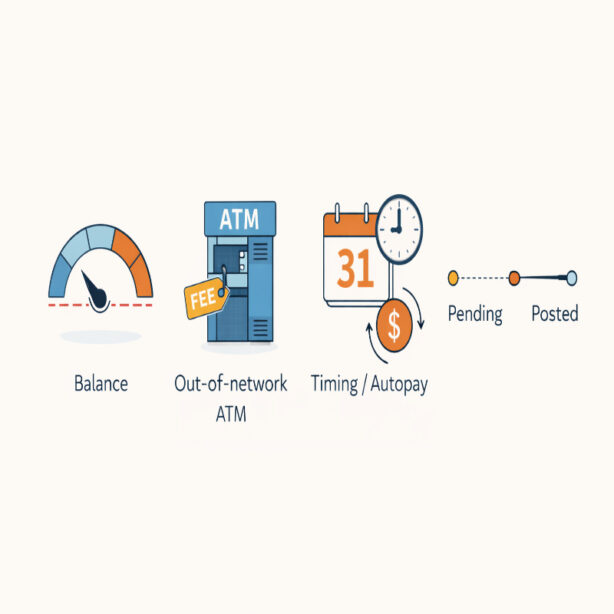

Most bank fees aren’t random. They’re triggered by specific conditions: your balance dipped below a minimum, you used an out-of-network ATM, a transaction posted earlier than you expected, or your account paid a charge you didn’t have funds for.

The tricky part is that these conditions can be easy to miss in real life. Deposits don’t always become available instantly. Autopays hit while you’re asleep. Subscriptions renew on odd days. And a bank’s “business day” timing can be different from the way you think about time.

So the goal here isn’t to memorize every fee. It’s to build a simple system for spotting the fee triggers and deciding whether a bank’s rules match how you actually live.

The fees that matter most (and the questions to ask)

Not every fee is equally important. Some are rare “once a year” annoyances. Others are repeat offenders that quietly drain checking accounts month after month.

Monthly maintenance fees

Monthly fees are the easiest to underestimate because they look small. But $10–$15 a month is real money over a year, especially if you’re also paying ATM fees or wire fees on top.

What to check:

- Is there a monthly maintenance fee? If yes, what is it?

- How do you waive it? Common waivers include minimum daily balance, a certain number of debit transactions, or direct deposit.

- Are the waiver requirements realistic for you? This sounds obvious, but it’s where people get stuck. A minimum daily balance waiver doesn’t help if your balance naturally swings.

If you’re someone whose income is irregular (freelance, commission, seasonal work), “easy to waive” often beats “low fee.” A low fee with a hard-to-hit waiver can be more expensive than a slightly higher fee that you reliably avoid.

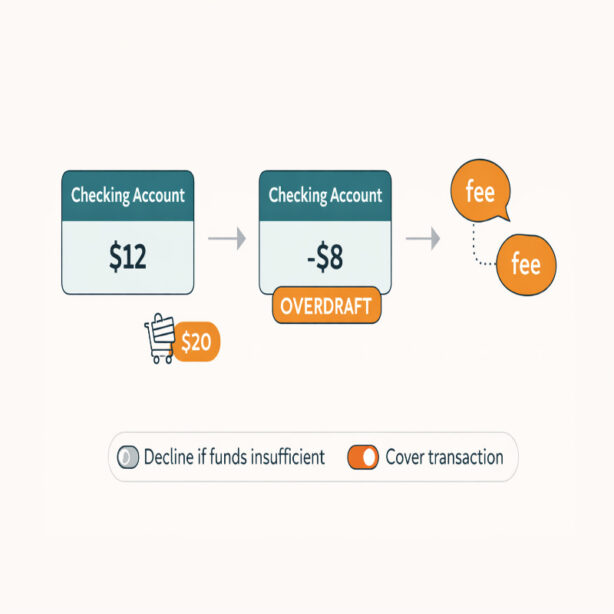

Overdraft fees (and the mechanics behind them)

Overdraft fees happen when a bank pays a transaction even though your account doesn’t have enough funds, which pushes your balance negative. Not all banks handle this the same way, and that’s exactly why it’s worth comparing.

Here’s a useful data point to calibrate your expectations: Bankrate’s survey has cited an average overdraft fee of $27.08 per overdraft transaction as of 2024. That number isn’t the point by itself, but it’s a reminder that one overdraft can cost more than the original purchase.

What to check:

- How much is the overdraft fee? Is it $0, $10, $35, something else?

- Is there a grace amount or “cushion”? Some banks don’t charge if you overdraw by a small amount.

- Is there a grace period? Some banks give you time to bring the balance back up.

- How many fees can be charged in a day? This is a big one. Multiple transactions can stack fees quickly.

- Can you opt out? In some cases, you can choose not to have certain transactions covered, which may mean the transaction is declined instead of triggering a fee.

There’s a “values” element here too, and I’m not going to pretend there isn’t. Some people prefer a bank to cover the transaction so rent doesn’t bounce. Others would rather have the transaction declined than pay a hefty fee. Neither is morally superior; it’s just your preference and your budget reality.

If you want the broader decision framework (fees plus access, safety, and support), jump back to the : what are some of the things you should look for when selecting the right bank?

Non sufficient funds (NSF) fees

NSF fees can happen when a bank declines a payment because you don’t have enough money in your account. Depending on the bank and the type of payment, you might see NSF fees, overdraft fees, or a mix of both.

What to check:

- Does the bank charge NSF fees? Some have reduced or eliminated them, while others still charge.

- Which transaction types trigger NSF fees? For example, ACH payments vs checks vs recurring bill pay.

- Are repeat fees possible? Some payments can be re-presented, and that’s where costs can multiply.

This is one of those areas where reading the account agreement is genuinely worth it. The rules can be specific, and you don’t want to learn them by accident.

ATM fees (the “small” fee that adds up)

ATM fees are sneaky because they come in layers. There’s what your bank charges for going out of network, and then there’s what the ATM owner charges. If you’re not paying attention, you can get hit twice.

What to check:

- Is there a fee-free ATM network? If yes, is it convenient where you live and work?

- Does the bank reimburse out-of-network ATM fees? If yes, how much per month, and what are the conditions?

- Do you travel? If you travel often, ATM policies matter more than you think.

In the pillar article, there’s a whole section on “Access and convenience” that connects ATM policy to real-world routines. If you want that perspective, it’s here: what are some of the things you should look for when selecting the right bank?

“Service” fees: wires, cashier’s checks, paper statements, and more

Service fees are the ones you don’t think about until you need them. Wiring money, getting a cashier’s check for an apartment, requesting a stop payment, asking for a paper statement, replacing a card quickly—these can all carry fees depending on the institution.

What to check:

- Wire transfer fees: Domestic vs international, incoming vs outgoing.

- Cashier’s checks: Fee per check, limits, and whether you can get one online or only in-branch.

- Paper statement fees: Many banks waive these if you go paperless.

- Inactivity fees: Less common now, but they still exist in some products.

If you’re choosing a bank for everyday life, you might not care about wires. If you’re paying rent via wire or moving money internationally, you absolutely do. Context matters.

The “true cost” method: a simple way to compare banks

If you want to compare banks in a way that feels concrete, estimate your true cost over a typical month, then multiply by 12.

Here’s a quick, realistic approach:

- List your likely triggers. For example: 2 out-of-network ATM withdrawals, 1 monthly maintenance fee if you miss the minimum balance, and maybe 1 overdraft every few months.

- Assign each a conservative number. If the bank’s fee schedule says $3 per out-of-network ATM plus the ATM owner fee, assume you’ll pay both sometimes.

- Calculate “good month” and “bad month.” Good month: no overdraft, no monthly fee. Bad month: one overdraft, one monthly fee, a couple of ATMs.

That “bad month” number is the one you should pay attention to. Because life is messy. It just is.

Also, don’t forget the psychological cost: if a bank’s rules make you constantly anxious about timing, holds, or fee triggers, that friction is real. It makes you second-guess normal spending.

How to read a fee schedule without losing your mind

Fee schedules and account agreements are long, but you don’t need to read them like a novel. You’re scanning for a few key sections:

- Monthly service fee and waivers

- ATM fees and reimbursement rules

- Overdraft/NSF fee amounts and limits

- Funds availability and holds

- Wire and special service fees

One tip I like: open two bank fee schedules side-by-side and search within the page for “fee,” “overdraft,” “ATM,” and “waive.” You’ll quickly see which bank is simple and which bank is… not.

If your primary concern is safety and account protection, the related cluster post goes deeper on that angle here: what to look for when selecting the right bank safety. Sometimes better security features (alerts, card controls) reduce the chance of costly mistakes.

Ways to reduce fees (even if you keep your current bank)

You don’t always need to switch banks immediately to reduce fees. Sometimes a few tweaks help a lot.

Set up alerts that prevent “surprise” moments

Low-balance alerts and transaction alerts can help you catch issues before they turn into overdrafts. If your bank’s app is good at this, use it. If it isn’t, that’s information too.

Build a small cushion (even a boring one)

A cushion balance is not exciting advice, and it doesn’t work for everyone, but it’s effective when it’s possible. Even $100–$200 sitting in checking can turn a would-have-been overdraft into a non-event.

Link a backup account (but read the rules)

Some banks offer overdraft protection that transfers funds from a linked account. It can be helpful, but it can also come with transfer fees or limits. Make sure you understand how it works before you depend on it.

Ask for a fee waiver (yes, really)

If you get hit with a fee and it’s unusual for you, call and ask politely whether it can be waived. It’s not guaranteed, but it’s often worth the five-minute attempt. Even if the answer is no, you’ll learn how the bank treats customers.

When switching banks is the smartest “fee strategy”

Sometimes the cleanest move is to choose an institution that simply doesn’t rely on the same fee model. Many banks have lowered or eliminated certain overdraft fees in recent years, while others still charge traditional amounts.

If you’re deciding between an online bank and a branch-based bank, it helps to compare their fee models alongside the convenience trade-offs. This related post is built for that: what to look for when selecting the right bank online vs traditional.

Just keep one thing in mind: “no fees” doesn’t automatically mean “best.” If fee-free comes with poor support, limited cash access, or confusing hold policies, you might be paying in frustration instead of dollars. That may be fine. Or it may drive you nuts. Only you know.

A quick mini-checklist before you open (or switch)

- Monthly maintenance fee: Amount and waiver rules.

- Overdraft fee: Amount, grace thresholds, daily limits, opt-out options.

- NSF fee: Amount and when it applies.

- ATM fee policy: Network access and reimbursement rules.

- Common service fees: Wires, cashier’s checks, paper statements.

- Reality check: Which of these are you likely to trigger in a normal month?

If you want the full selection framework (not just fees), the pillar article is still the best “start here”: what are some of the things you should look for when selecting the right bank?

Because fees are only one piece. But they’re a piece that tends to show up again and again—quietly—until you fix it.